KENNIS BLOG

Digital payment services:

FinTech and financial supervision

6 June 2024

In the dynamic world of financial technologies (FinTech), digital payment services have become a daily occurrence. Paying online via, for example, iDeal, Tikkie or Paypal. These services, ranging from digital wallets to entire online payment platforms, have dramatically changed the way people manage money and make payments. Although this makes online payments easier, it has actually only become more complicated from a legal point of view.

In this blog, we will take a closer look at the legal framework behind these digital payment services. What are digital payment services? How can you differentiate between the different institutions? And how strict is its financial supervision?

The Payment Chain

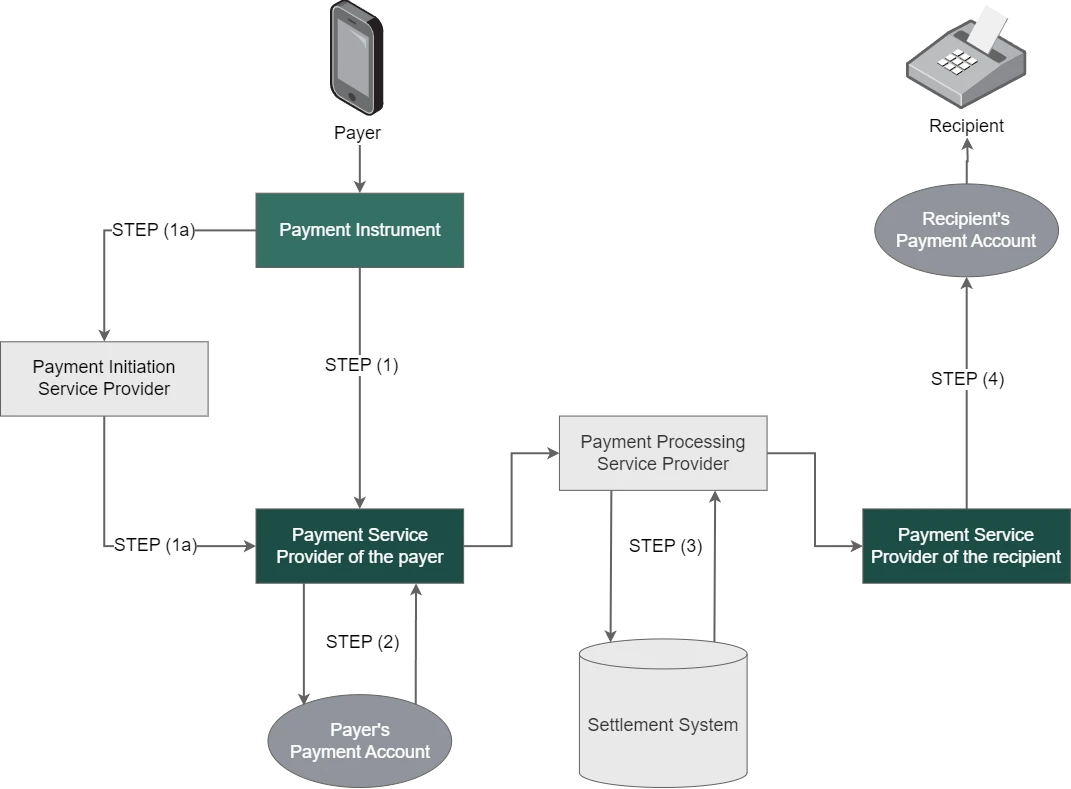

To get a better idea of the different payment services out there, it is useful to first get an overview of the payment chain. Below is a typical SEPA payment[1] :

- Step 1: The payment starts with the initiation. To do this, the payer needs a payment instrument. This can be pretty much anything you can use to initiate a payment order, such as a mobile banking app or a debit card. The payment order itself contains all the relevant information, such as the amount and the beneficiary's bank account.

- Step 1a: This first step is also where many FinTech companies are active. Companies such as iDeal and Payconiq make it very easy to initiate payment orders. For example, the correct amount and bank account of the beneficiary are automatically entered when paying on a webshop. In this way, sending the payment order is made increasingly easy.

- Step 2: The payment order is then received by the payer's payment service provider. This is often the bank where the payer holds its payment account. This payment service provider then carries out a number of checks. For example, it checks whether the payment order also contains all the necessary information and whether there are enough funds in the account. If all checks are successful, the amount will be deducted from the payer's payment account.

- Step 3: Payment service providers of both the payer and the recipient are affiliated with a so-called settlement system. These are systems that settle payment transactions between payment service providers (often banks). The settlement system is managed by an independent organisation in which the banks themselves, in turn, hold an account. This organization is called a 'Payment Processing Service Provider', such as VISA or Mastercard. All the different transactions come in here and are settled with each other. Thus, the payer's payment service provider, after carrying out its own checks, sends a message to a payment processing service provider, which then enters into the settlement system that a payment is being made from one payment service provider to another.

- Step 4: The recipient's payment service provider will then receive a message from the settlement company, containing the details of the payment that has been made. The latter will then credit money to the recipient's payment account based on the information it has received from the settlement company.

What are Digital Payment Services?

Digital Payment Services is actually a collective term for services that a company could offer (online/digitally), such as online payments and a digital wallet. Previously, many of these services were provided by a bank, but with the rise of 'open banking', these services have become more disaggregated and can be more easily provided by (third-party) FinTech companies. A "Payment Service" is legally defined in the Payment Services Directive 2, or "PSD2".[2] It also makes it clear what different payment services there may be. This includes:

- Managing a payment account: Managing a payment account is generally associated with a traditional bank, but with the rise of open banking and new FinTech companies like Monese, it no longer has to be that way. FinTech companies are constantly looking for ways to modernize payment account management.

- Carrying out payment transactions on a payment account: This involves transferring money to a payment account. This is not about initiating the payment order, but about its actual execution. These types of transactions are also associated with the traditional bank.

- Account information services: these are services that only provide information about the underlying account. For example, CashFlow, a product from Inverse that focuses on providing automated financial planning and cash flow management. It uses account information to provide insight into the financial situation of businesses and individuals.

- Withdrawing and depositing cash: in order to be able to put cash in a payment account, one will have to go to a physical location. FinTech companies like Monese therefore enter into contracts with local offices that receive the money for them, offering the services of traditional banks in a modern and cost-efficient way.

- Initiation of (internet) payments: think of iDeal or Payconiq (now both part of the European Payments Initiative), which ensure that consumers can easily pay in (web) shops. The bank account itself is not held with iDeal or Payconiq. These companies only work as intermediaries and initiate the payment order, as shown above in Step (1a). Of course, you can also initiate the payment order yourself by filling in a form in your online banking environment, but these types of FinTech companies make the initiation a lot faster and easier.

- Issuance of payment instruments: where the payment instrument used to be mainly the debit card, nowadays it is increasingly an app or digital wallet. These apps and wallets are payment instruments issued by companies such as Payconiq, SumUp and Tikkie .

- Acceptance of payment transactions: especially with webshops, it is important to be able to easily accept and process payment transactions, so that a smooth transfer of funds to the beneficiary occurs. If, for example, you can pay with Payconiq on a webshop, Payconiq will provide the service of acceptance and processing of the payment transaction for the webshop.

- Money remittances: this is a payment service that allows you to transfer money directly to a beneficiary, provided by companies such as MoneyGram and Western Union. This is often used to transfer money to someone where a regular bank transfer is not easy. Normally, therefore, money remittances are used to transfer money to a beneficiary abroad. This may be because there is a long processing time between banks that cannot be waited for or because the beneficiary does not have their own bank account at all. Payment institutions providing money remittances also don't open a payment account for you. The payment institution only receives the money (by bank transfer or cash) and passes it on to the beneficiary (again by bank transfer or in cash at its office in the beneficiary's country).

What is Open Banking?

Open banking is a concept that revolves around sharing financial data from bank accounts with third-party financial service providers via APIs (Application Programming Interfaces). This principle is embedded in PSD2[3] and allows consumers to give third parties access to their financial data, with their explicit consent of course.

The idea behind open banking is to encourage more competition and innovation in the financial sector by making it easier for new players to access financial data. This allows consumers to benefit from a wider choice of products and services that better meet their needs. This has led to an explosion of new players in the market, such as Fintech companies offering payment initiation and account information services. As a result, the work of one all-encompassing institution (a bank) has been divided into smaller services that can now be carried out by specialised FinTech companies.

Payment Institution or Credit Institution?

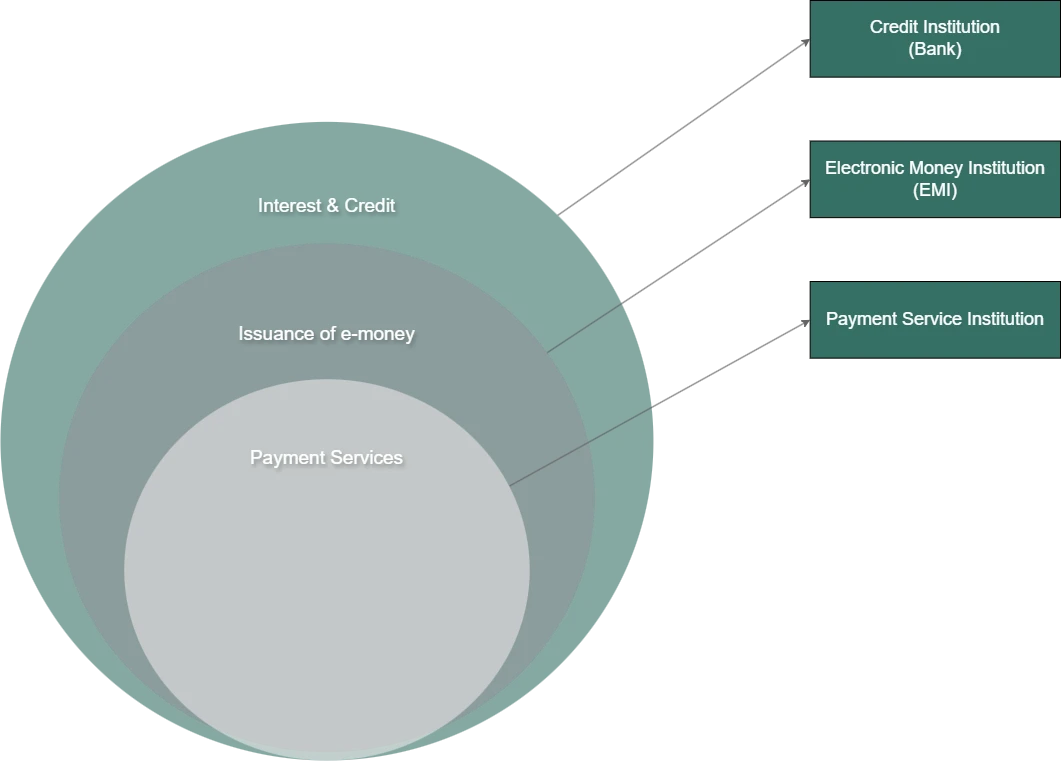

At both the national and European level, various terms are used to describe payment service providers, such as electronic money institution, payment institutions and credit institutions. These different designations can be confusing even for professionals, let alone outsiders to the financial world. At the same time, understanding these definitions is essential for financial supervision, as they determine which supervisory regime applies to a company. This is important to ensure the security of financial transactions. In particular, due to the rise of FinTech companies in recent years, which often offer different financial services, it is becoming increasingly difficult to place these companies in clear categories. It therefore remains a challenge for legislators and regulators to ensure that legislation is kept up-to-date and enforcement is effectively implemented. In this blog, I won't go into detail about the differences between these terms, but I will try to give a sketchy summary of them.

Let's start with the biggest player – a bank, also known as a credit institution. If it is possible to deposit or withdraw money to and from a payment account where you can get interest or credit, then we are dealing with a bank. This forms the basis for executing transactions. Once you have a payment account, you can put money into it, but the transaction itself is made up of several components. If a company only wants to perform one of these components, without actually keeping money for you in a bank account, then we are dealing with a payment institution. These are companies that offer payment services, as described earlier. This includes services for providing account information and initiating payments. So, a payment institution is not always a bank, but a bank is always a payment institution. Accordingly, a banking license encompasses a wide range of activities. The license of a payment institution, on the other hand, is 'smaller', because it encompasses less than a banking license. The financial supervision of payment institutions is therefore logically less demanding. However, it is more difficult to distinguish between a bank and an electronic money institution.

The Electronic Money Institution

Now let's look at another player: the Electronic Money Institution (or 'EMI'). Although both a bank and an EMI were previously included in the definition of 'credit institution', the European legislator has revised the rules for EMIs in order to facilitate market entry and promote innovation. As a result, EMIs have become a type of institution in their own right. This type of institution issues electronic money in exchange for scriptural money, which can then be used for payments to various parties. Unlike a bank, an EMI does not (or no longer) keep the deposited money under the same strict regulation as a bank. EMIs, like payment institutions, are no longer subject to liquidity requirements. However, they still need to comply with specific regulations and need a license to offer these services. The conditions for such a licence have also largely been brought in line with those of a payment institution. An exception to this licensing requirement is electronic funds with limited uses (such as a gift card to shop at one particular store),[4] or if no more than 3 million euros in transactions are made annually.[5]

Similar to a payment institution, EMIs can offer a variety of services, including the provision of payment cards or the facilitation of digital payments through mobile apps or online platforms. These institutions often play an important role in facilitating electronic transactions and can be attractive to consumers and businesses looking for alternatives to traditional bank accounts. This often does not require a separate permit, as this will be included in the existing permit of the EMI.[6] Ultimately, the European Commission's aim is to integrate the payment institution and the EMI into a single institution in the longer term.

What is Electronic Money? And is it safe?

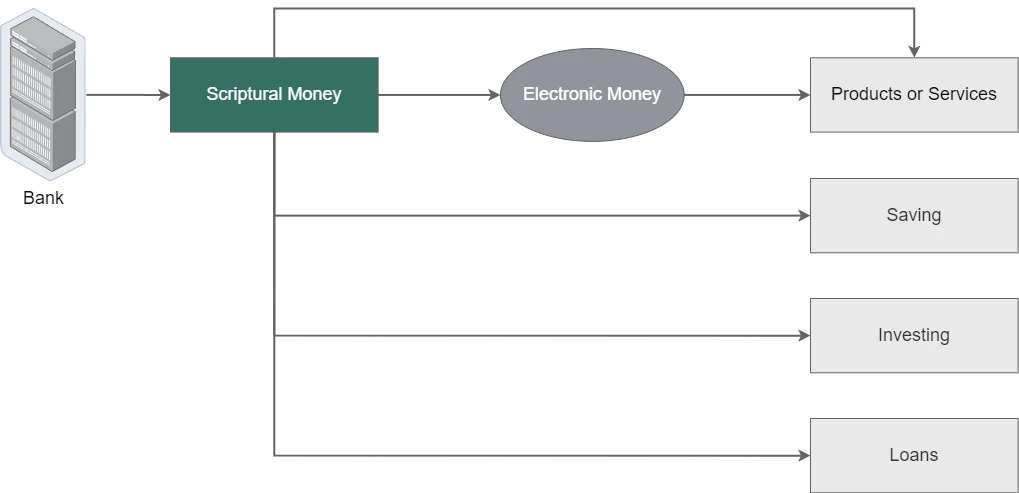

An important question that arises is what exactly is meant by 'electronic money'? Isn't the scriptural money that is at the bank and visible online also just 'electronic money'? So what is the difference with an EMI?

The definition of electronic money has been revised in the E-money Directive (EC) 2009/110 (E-money Directive) and is now quite broad. This means that both money on a plastic card (such as a gift card) and electronic money stored on a central server fall within the scope of the definition. As a result, scriptural money could perhaps also be seen as electronic money, but the law makes a distinction between them. The distinction is mainly in the order and use of it. With cash or scriptural money, electronic money can be purchased as a means of payment. This purchased electronic money has a limited function. It can only be used as a means of payment for products or services. An EMI will therefore not be able to give you interest or credit, as a bank can.[7] The electronic money will therefore also always have to be paid in advance (otherwise it will become a credit). There can't even be a direct debit afterwards. So you can think of it as a kind of prepaid credit, which you can spend in many places.

However, an important difference is that because money issued by an EMI is not classified as scriptural money, it is also not considered a deposit. As a result, an electronic money wallet with an EMI is not covered by the deposit guarantee scheme, while this does apply to bank accounts in the EU. The deposit guarantee scheme is a scheme designed to protect account holders' money if a bank fails (up to a certain amount). Therefore, if an EMI goes bankrupt, account holders are not entitled to compensation from the deposit guarantee scheme for the money they have stored in their wallets. However, there is another form of protection. An EMI must secure the money they hold in these wallets (also known as the 'float'). They do this by not mixing these funds with the funds of other creditors, such as financiers of the EMI. In the Netherlands, this practically means that the money is held in a bank account that is in the name of an independent third-party funds foundation (stichting derdengelden).

EMIs are also currently outside the resolution regime that has been put in place to bail out banks (and insurers) in the event of imminent failure. This means that there will be no bail-outs for EMIs. The reasoning behind this is that banks play an essential role in the stability of the economy, while EMIs do not. They are not so closely intertwined with the economy that they are indispensable. Nevertheless, bank accounts are essential for numerous economic activities in our society. Even an EMI, or its third-party funds foundation, needs a bank account to secure its money.

Emerging changes

Although many new laws and regulations have been introduced in the field of (digital) payment services in recent years, there seems to be no end in sight. A lot of harmonisation (and simplification) is needed to ensure that legislation is as modern and clear as the FinTech it regulates. In 2023, the European Commission made a proposal to merge PSD2, the Electronic Money Directive and the Settlement Finality Directive 98/26/EC into one new directive, the 'Directive on Payment Services and Electronic Money Services in the Internal Market' or PSD3.[8] The Commission's proposal focuses on the provision of payment services and e-money services, with a specific focus on the authorisation and supervision of payment institutions. It comes after a thorough review of PSD2 in 2022, which found that adjustments were needed to improve the effectiveness of the directive.

This initiative is in line with broader EU strategies, such as the EU Digital Finance Strategy, which aim to promote digital innovation in the financial sector and strengthen the internal market for financial services. The proposal is also supported by other relevant legislation, such as the Single Euro Payments Area (SEPA) Regulation and the General Data Protection Regulation (GDPR). The proposal for a revision of PSD2 is expected to generate debate within the EU institutions and stakeholders in the financial sector.

Conclusion

Offering digital payment services is an exciting yet challenging field for FinTech companies. In addition to developing innovative technologies and attracting customers, these companies must also comply with a complex web of laws and regulations. By working closely with legal experts and remaining proactive in monitoring changing regulations, FinTech companies can operate successfully within this legal landscape and continue to contribute to the growth of the digital economy.

[1] SEPA stands for 'Single Euro Payments Area' and is a European project that has brought a lot of laws and regulations to life to harmonise and facilitate payments between banks in Europe.

[2] Directive EU/2015/2366. For more information on PSD2, see https://www.dnb.nl/voor-de-sector/open-boek-toezicht/wet-regelgeving/psd2/

[3] Art. 35 and 36 PSD2.

[4] Art. 1:5 Financial Supervition Act (Wet op het financieel toezicht – ‘Wft’).

[5] Art. 1a Exemption Scheme under the Financial Supervision Act (Vrijstellingsregeling Wft).

[6] Section 2:3a(2) of the Financial Supervision Act.

[7] Section 4:31 of the Financial Supervision Act.

[8] https://eur-lex.europa.eu/legal-content/NL/TXT/?uri=CELEX:52023PC0366

Do you require legal assitance on this topic? Then please click below to get in touch.